Palm Beach Waterfront Flood Insurance & Buyer Tips

April 16, 2026

April 16, 2026

Buying waterfront in Palm Beach can feel simple at first glance. You find the view, the dock, the layout, and the lifestyle you want. Then flood-zone questions show up, and suddenly the decision gets more technical. The good news is that with the right information, you can sort through the risk, the insurance questions, and the property details with much more confidence. Let’s dive in.

For waterfront buyers in Palm Beach, flood maps are not a minor detail. They can affect insurance costs, lending requirements, renovation plans, and how you compare one property to another.

That matters even more now because the Town of Palm Beach’s current Flood Insurance Rate Maps became effective on December 20, 2024. According to the Town of Palm Beach Planning, Zoning & Building information, the updated maps are in use now, and Palm Beach County says the same revision moved thousands of eastern-county properties into higher-risk categories, with more than 16,000 parcels seeing Base Flood Elevation increases of one foot or more.

Palm Beach County also makes an important point for buyers: flood risk exists countywide, and windstorm insurance does not cover flood damage. If you are shopping oceanfront, Intracoastal, or other waterfront property, that is a key part of your budget and due diligence.

One of the most common buyer mistakes is mixing up flood zones with hurricane evacuation zones. They are not the same thing.

Palm Beach County’s official emergency management guidance says you should know your evacuation zone separately from your flood zone. A home can sit in one evacuation zone and a completely different FEMA flood zone. For a waterfront buyer, that means you need to check both instead of assuming one answers the other.

This matters because flood-zone status is tied to insurance and building standards, while evacuation zones relate to storm-preparedness planning. Both are important, but they answer different questions.

The official public source for flood-hazard maps is FEMA’s Flood Map Service Center. On those maps, you can see flood-hazard zones, Special Flood Hazard Areas, Base Flood Elevations, and in some cases floodways.

For Palm Beach buyers, the flood map is the starting point, not the final answer. It tells you the mapped risk category, but you still need to compare that map data to the home’s actual elevation and building features.

Zone AE is a detailed 100-year floodplain where Base Flood Elevations are shown at selected intervals. FEMA classifies AE as part of the Special Flood Hazard Area.

If a home is in AE, the big question is not just that label. You also want to know how the home’s lowest-floor elevation compares with the mapped BFE.

Zone VE is a coastal high-hazard zone with added storm-wave hazard. FEMA includes VE in the Special Flood Hazard Area, and mandatory flood-insurance purchase requirements generally apply when there is a mortgage from a government-backed lender.

For Palm Beach waterfront buyers, VE often deserves extra scrutiny because coastal surge and wave action can create stricter building concerns. Features like elevated construction and breakaway walls may become especially relevant.

Zone X usually refers to areas outside the 500-year floodplain or places with relatively shallow flooding, and no BFE is shown on the map. That can sound reassuring, but it should not be read as no risk.

FEMA specifically says there is no such thing as a no-risk flood zone. In practice, Zone X means lower risk, not zero risk. That distinction is especially important near the coast, where property-specific insurance pricing can still be meaningful.

When you are evaluating a waterfront property, the smartest approach is to compare more than the zone name. In many cases, the more useful questions are:

FEMA defines BFE as the elevation of the 1% annual-chance flood. According to FEMA’s guidance on flood mapping and elevations, the practical buyer test is often zone label versus actual building elevation, not zone label alone.

An elevation certificate can help you understand how a structure sits relative to the mapped flood risk. In Palm Beach waterfront transactions, that can be one of the most useful documents in the file.

Florida now maintains a statewide digital elevation-certificate system. Since January 1, 2023, surveyors and mappers must submit digital copies to the state, which gives buyers another path to search for a certificate if it is not readily available from the seller.

Palm Beach County also notes that staff may be able to help determine whether an elevation certificate is on file for certain properties and whether other floodplain concerns may affect renovation plans. That is one reason serious waterfront buyers should ask for this early, not after inspections are already underway.

Flood insurance is a separate policy. FEMA states that most homeowners insurance does not cover flood damage, and homes in high-risk flood areas with mortgages from government-backed lenders are generally required to carry flood insurance.

FEMA also notes that NFIP coverage usually has a 30-day waiting period unless the policy is required by a lender or tied to a map change. If you are buying on a tight timeline, that timing can matter.

Just as important, lenders can still require flood insurance outside high-risk zones. So even if a home is not in AE or VE, you should not assume coverage will be optional until your lender confirms its requirements.

Under FEMA’s Risk Rating 2.0 approach, premiums are more property-specific than zone-specific. FEMA says pricing can consider:

For buyers, that means two nearby waterfront homes in the same general area may not insure the same way. A mapped zone is still important, but it is no longer the whole story.

One bright spot for buyers is the Community Rating System, or CRS. FEMA says participating communities can earn NFIP premium discounts ranging from 5% to 45%.

The Town of Palm Beach says it is a Class 6 CRS community, and NFIP policyholders receive a 20% annual discount. Palm Beach County says unincorporated property owners receive a 25% discount. Those savings can make a real difference, but they vary by community, so you should verify the discount for the exact municipality where you are buying.

Waterfront buyers should also look beyond the map and inspect the way the home is built. Certain mitigation features can affect safety, compliance, insurability, and long-term costs.

Common coastal features described in the research include:

FEMA defines a breakaway wall as a non-structural wall intended to collapse without damaging the elevated part of the building. Florida CRS guidance also notes that machinery and equipment should be elevated to the same level as dwellings, and Florida code adds at least one foot of freeboard for many homes.

If a home has been updated, you will want to know whether those updates were properly permitted and whether the improvements align with current floodplain requirements.

A beautiful waterfront property can still bring surprises if you plan to remodel. Palm Beach County warns that floodplain work generally needs a permit and that no construction, including earth-moving, is legal in a floodplain without one.

The county’s flood information resources also note that buyers in some areas may want help checking whether a parcel could be affected by coastal erosion, whether substantial-improvement rules might apply before a major renovation, and whether local records already contain relevant flood documents.

This is especially important if you are buying for a cosmetic update, large addition, or full renovation. The purchase may make sense, but only if the floodplain rules still work with your plans.

For Palm Beach waterfront buyers, the safest process is to verify every key piece of flood information before you commit. The Town of Palm Beach provides downloadable flood maps and a flood-zone determination system, and Palm Beach County recommends confirming flood information with a licensed engineer, architect, or surveyor before purchase or construction.

Here is a simple checklist to use:

Flood zones should not automatically rule out a Palm Beach waterfront property. They should help you ask better questions.

In some cases, a higher-risk map zone may be balanced by strong elevation, solid mitigation features, and acceptable insurance pricing. In other cases, a lower-risk label may still come with costs or limitations that affect your comfort level. The goal is not to panic or assume. It is to compare each property clearly and make a decision based on verified facts.

If you are considering waterfront property in Palm Beach, West Palm Beach, Delray Beach, Boca Raton, or nearby coastal communities, having patient guidance can make the process much easier. Abbey Adair takes an education-first approach so you can understand the details, ask the right questions, and move forward with confidence.

Stay up to date on the latest real estate trends.

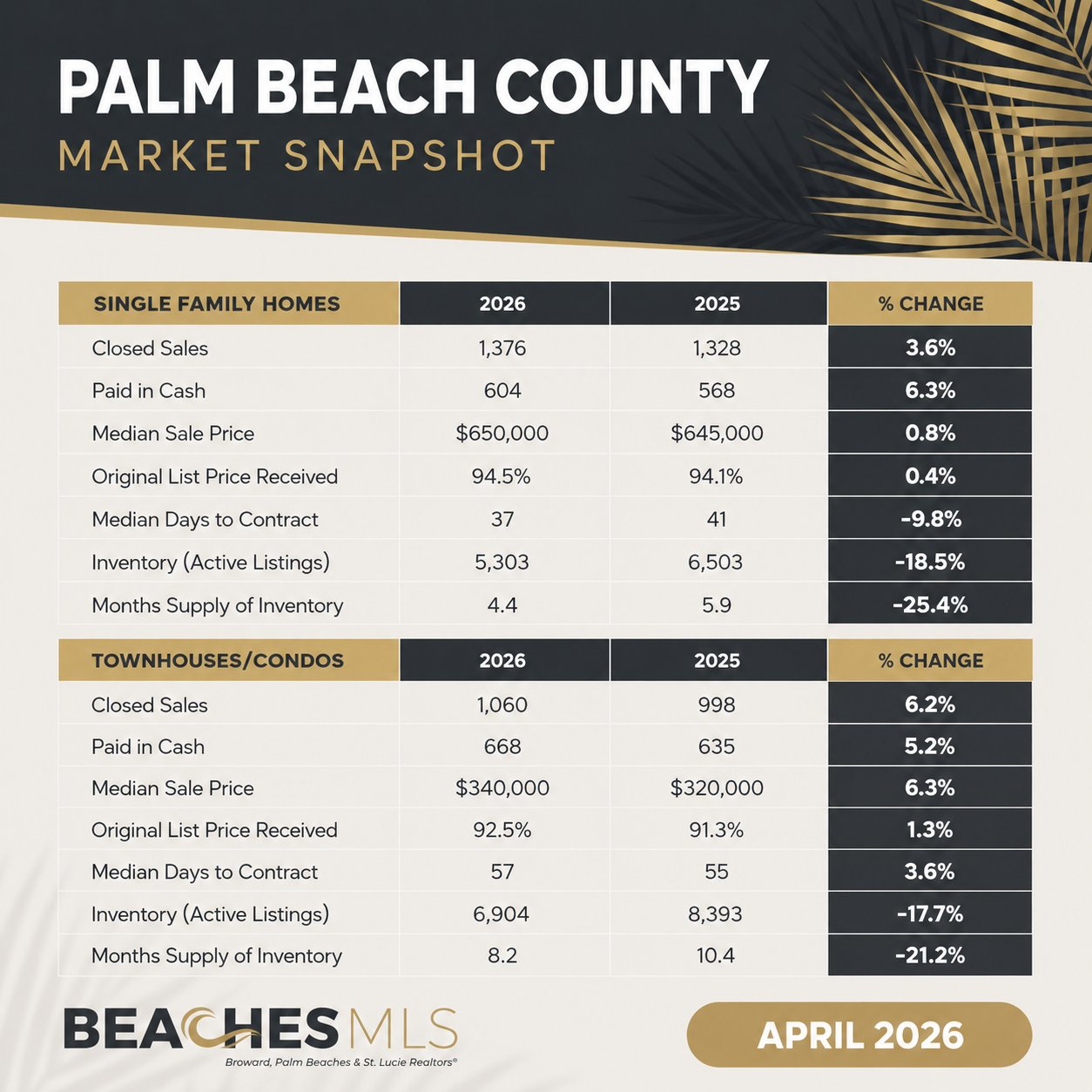

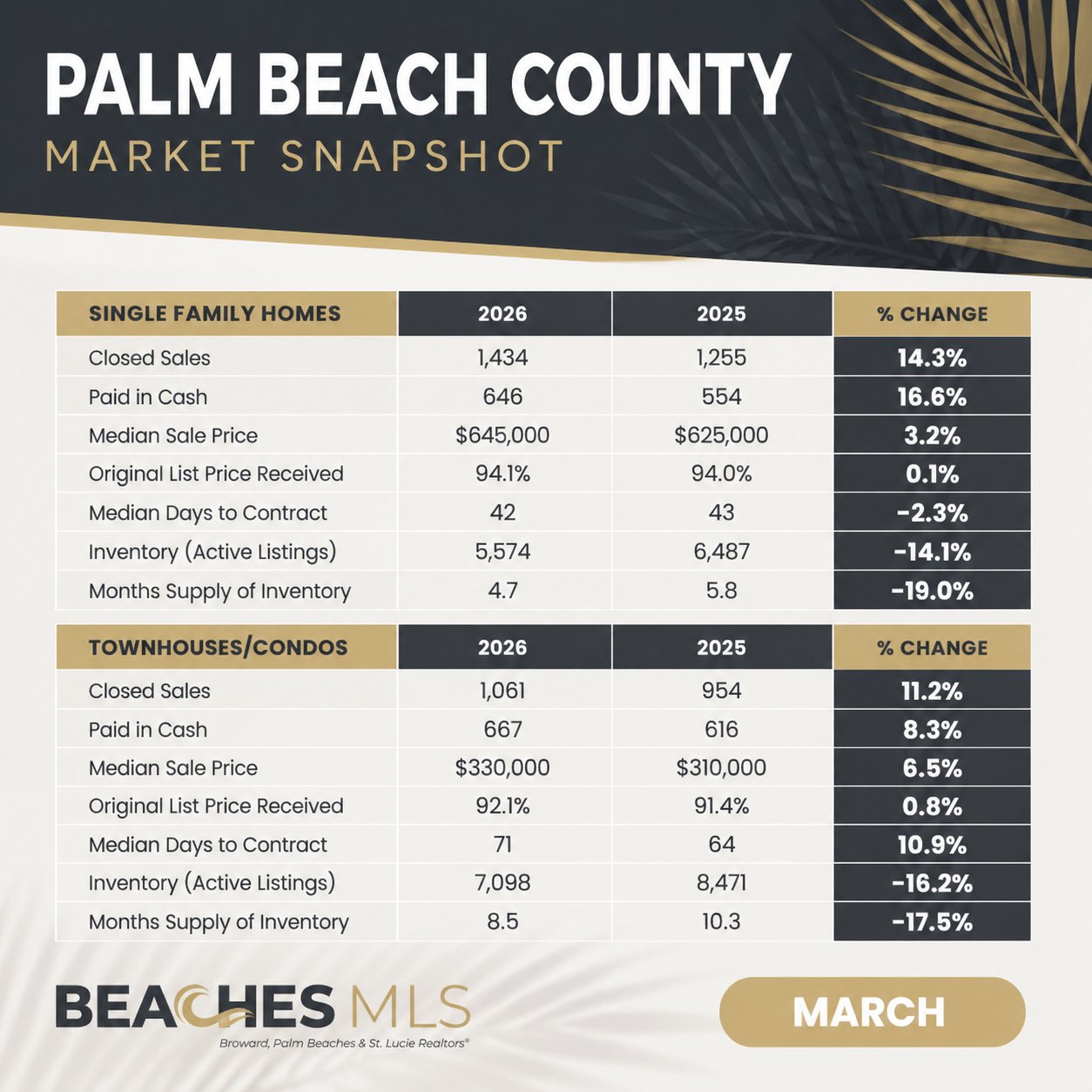

Market Update

Market Update 03/2026

Embarking on a real estate journey can be daunting, but you don't have to do it alone. With my unique blend of educational insight and real estate expertise, I'm here to guide you through every step, ensuring a smooth, informative, and successful experience. Ready to get started? Contact me today, and let's make your real estate dreams a reality.