Palm Beach Oceanfront Condos Or Estates: How To Choose

March 12, 2026

March 12, 2026

Choosing between an oceanfront condo and a private estate in Palm Beach can feel like picking between two great lifestyles. You want the water, the sunshine and a smooth ownership experience. This guide gives you a clear, side‑by‑side look at price levels, costs, rules and resale so you can choose with confidence. Let’s dive in.

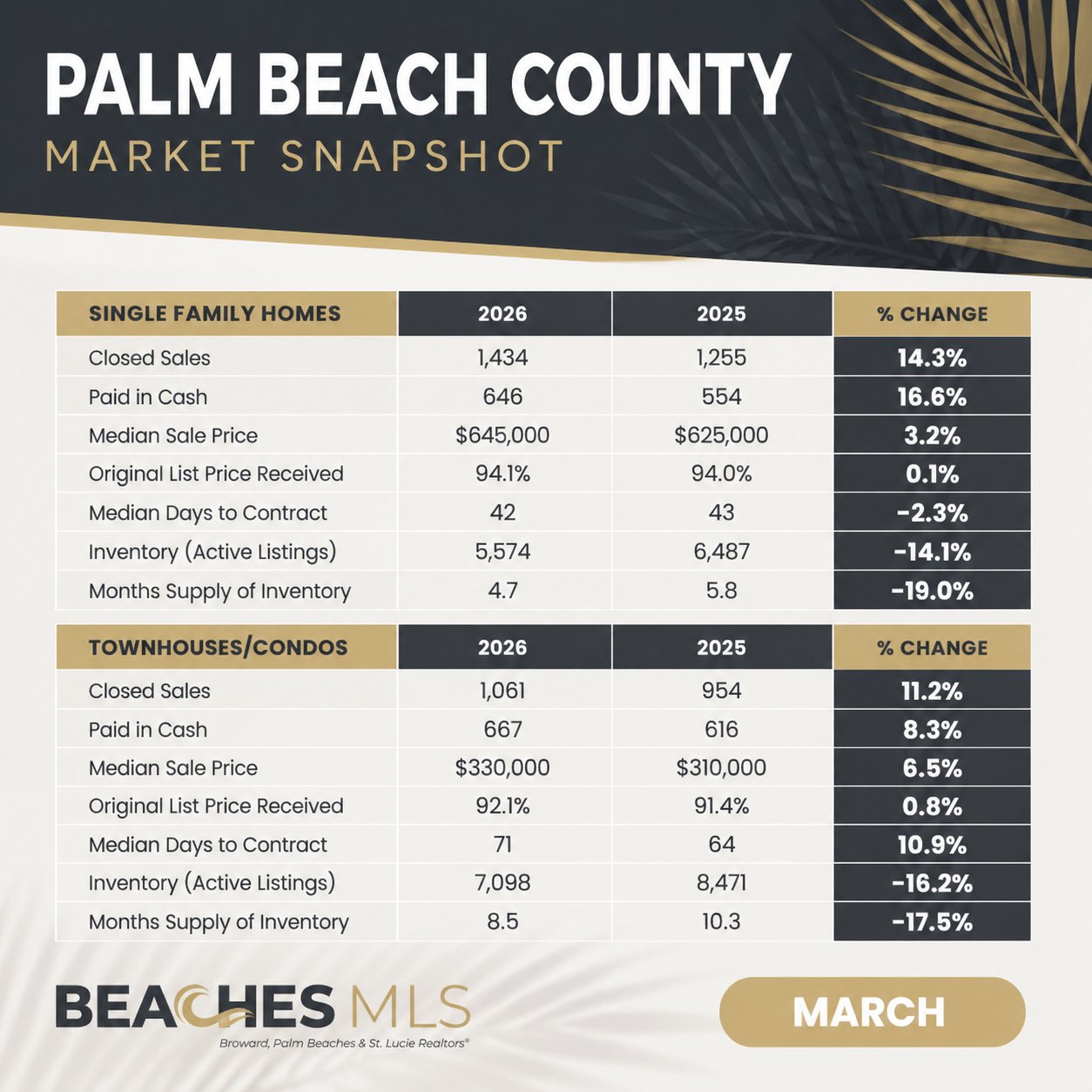

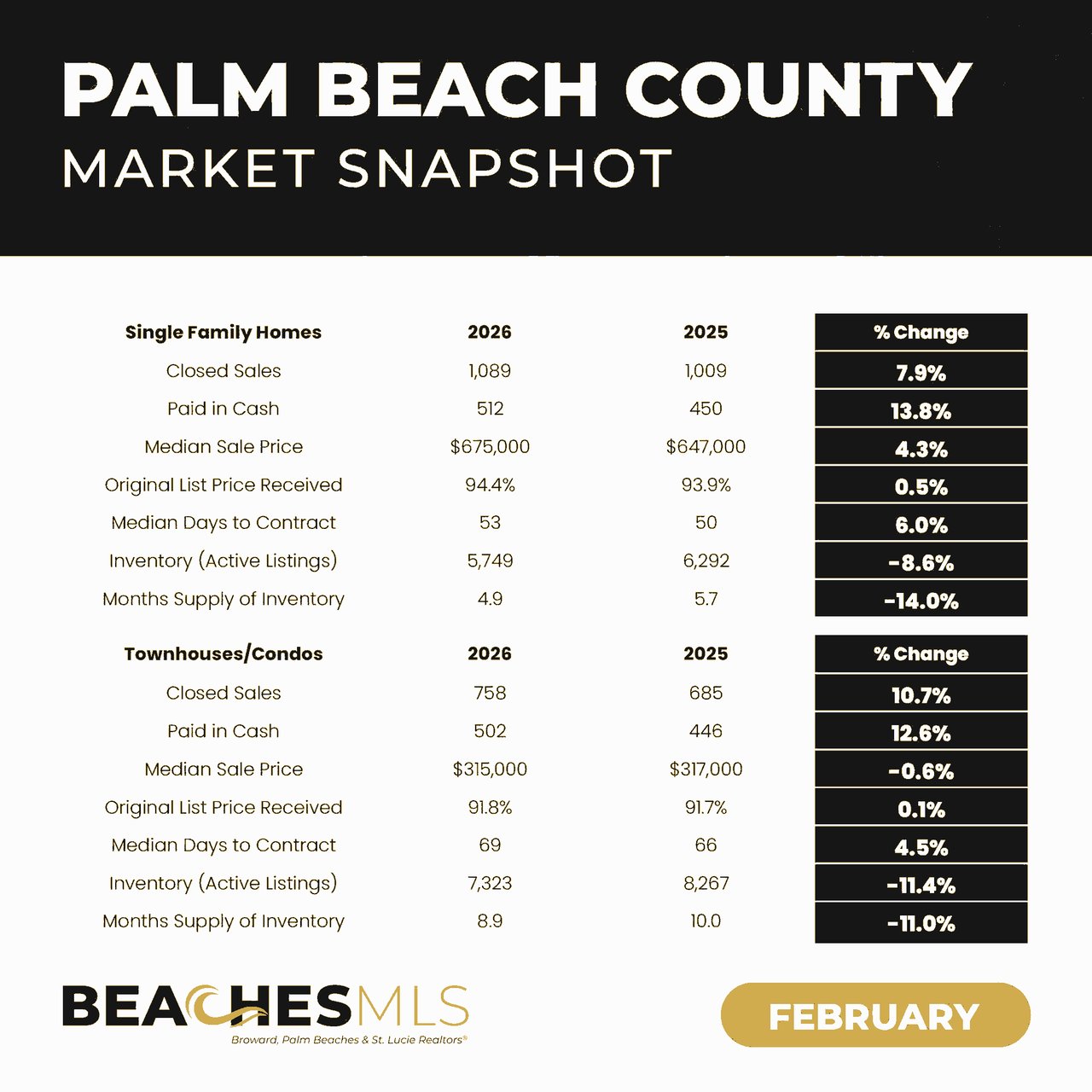

Palm Beach island has one of the widest gaps between condo and single‑family prices in South Florida. In Q1 2025, the median condo sale price was about $1,500,000, while the median single‑family sale price reached about $13,950,000 on the island, according to the latest Elliman report for the Town of Palm Beach. You also see different inventory patterns between the two property types, and many high‑end single‑family sales close with cash, which affects speed and terms for buyers and sellers. You can review the quarterly medians, months of supply and commentary in the same report to understand seasonality and liquidity on the island.

Condos concentrate convenience. Many oceanfront buildings include building insurance through a master policy, staffed security or front desk, common‑area maintenance, and amenities like pools and fitness rooms built into your monthly dues. If you travel often or prefer turnkey living, this can be a strong fit. Renovations and rentals are regulated by the building’s rules, so your project scope and timelines may be more structured.

Estates deliver privacy and control. You decide your design, guest capacity, and vendor roster, and you can plan spaces for boats, cars or staff as zoning allows. Ownership is more hands‑on since you manage grounds, pool, mechanicals and security directly, often with help from a household or estate manager. If you value freedom, outdoor space and privacy, a fee‑simple home can be the right platform.

Florida’s coastal market carries higher insurance costs than many inland areas. Recent state market summaries note that Palm Beach County premiums average in the mid‑$5,000 to low‑$7,000 range for typical single‑family homes, with beachfront exposure often requiring higher premiums or private placement. Condos share building coverage through the association’s master policy, but you still need a unit policy for finishes and contents. Review current insights in the state market overview. See Florida insurance market context.

Flood insurance is a key distinction. Standard NFIP policies cap coverage for a 1 to 4 family residence at up to $250,000 for the building and up to $100,000 for contents. Those limits are usually far below replacement cost for luxury oceanfront homes, so private flood or excess coverage is common for estates. Check NFIP limits and guidance.

The Town of Palm Beach outlines how millage layers work and provides example calculations that show how assessed value, exemptions and each levy create your total ad valorem tax. The town’s municipal millage is one layer in a larger county and school stack, so parcel‑specific lookups are best when you are under contract. Review the Town of Palm Beach tax overview and examples.

A common planning rule is to set aside about 1 percent of a home’s value per year for routine maintenance, with a practical range of 1 to 3 percent or more for older, complex or ocean‑exposed properties. This is a baseline for recurring work and does not include major capital projects. See a plain‑English guide to maintenance budgeting.

Staffing is a major line item for larger homes. In South Florida, full‑time estate or household managers often earn about $125,000 to $250,000 or more depending on scope. Additional staff like housekeepers, chefs, drivers and security add to payroll and benefits. Review regional staffing ranges for Palm Beach.

Florida condominiums are governed by Chapter 718 of the Florida Statutes. Associations maintain common areas, collect assessments and carry a master insurance policy. Before you buy, review the declaration, bylaws, rules, reserves and any recent or pending special assessments. Typical rules to confirm include rental minimums, guest policies, renovation scope and timing, and buyer approval steps. Read the Florida Condominium Act overview.

If you plan significant customization, estates provide the most control, subject to local codes and preservation rules where applicable. Historic or landmarked homes can involve additional review, so your due diligence should include the property’s status and any design restrictions.

On the island, high‑end single‑family homes often sell for cash and some trade privately off market. Condos can be active at certain price points but may show higher months of supply in softer quarters. Review recent quarters for your specific segment to set expectations on timing, pricing and negotiation strength. Scan recent medians, days on market and months of supply.

Use these prompts to decide which path fits you best:

Lifestyle and time

Budget and carrying costs

Resale horizon and liquidity

Storm and flood risk tolerance

Operations and staffing

When you add these up side by side, one option usually clicks with your lifestyle and comfort level.

Ready to explore both paths on the island and nearby coast? Reach out to schedule a private tour plan and a tailored cost worksheet. You will get clear numbers, building packets or vendor quotes, and a step‑by‑step timeline from offer through close. Connect with Abbey Adair to get started.

Stay up to date on the latest real estate trends.

Market Update 03/2026

Housing Market Update

Embarking on a real estate journey can be daunting, but you don't have to do it alone. With my unique blend of educational insight and real estate expertise, I'm here to guide you through every step, ensuring a smooth, informative, and successful experience. Ready to get started? Contact me today, and let's make your real estate dreams a reality.